Consumer Confidence Sequel: Two Thumbs Up

Biden receives perhaps his best piece of news in 2024

Two weeks ago, I wrote that despite a December surge in consumer confidence, the widely followed Index of Consumer Sentiment from the University of Michigan was still far below where it should be.

I didn’t expect to have to update the post so soon. But today, in what was arguably the 2024 news item most likely to affect the November election, the University of Michigan reported consumer sentiment surged again. The preliminary results for January show its index rose a startling 9.1 points to 78.8.

This was the biggest monthly rise since December 2005. More impressively, it immediately followed an 8.4 point December rise that also was the biggest monthly rise in consumer sentiment since December 2005.

When it comes to consumer confidence, resistance is stronger than momentum. Big jumps like the one we saw in December are usually followed by a decline and almost never followed by another big gain. Together, the two-month increase in consumer confidence is the biggest since 1991.

What’s going on? It’s always dangerous to draw too many conclusions from a month or two of economic data. But it’s possible that consumers just might be starting to accept this reality: Our economy is in pretty darn good shape.

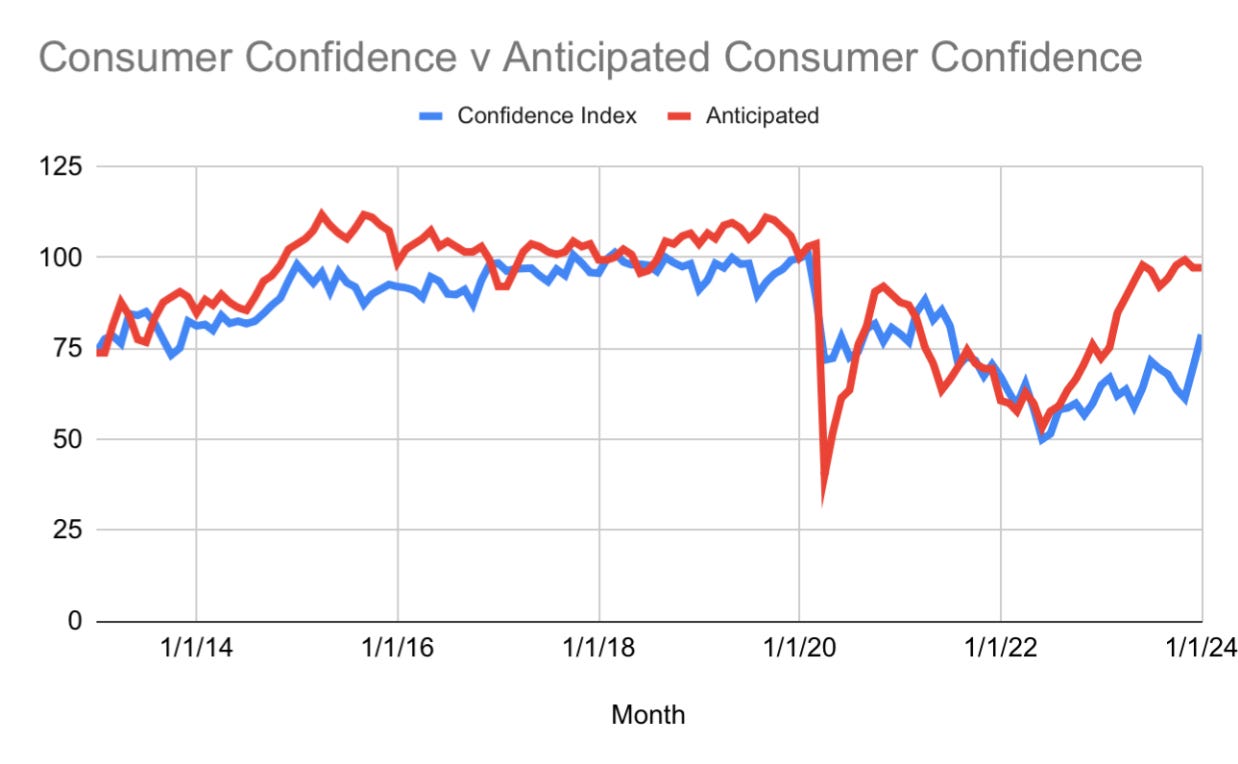

This chart is almost identical to the chart I posted two weeks ago, updated to add the month of January 2024. The red line shows what I call Anticipated Consumer Confidence - a measure of where consumer confidence “should” be, based on the inflation and unemployment rates (the so-called Misery Index). Anticipated confidence began to soar in spring 2022. But actual consumer confidence rose much more modestly, leaving a massive gap between actual and anticipated consumer confidence for most of 2023.

For an explanation of how I calculated the anticipated confidence number, please see the end of my post from two weeks ago.

This gap was unlike anything we’ve seen in at least a decade, and it’s been a source of equally massive frustration in the Biden administration and for anyone who would like to see him re-elected. As I said two weeks ago, no presidential candidate from the incumbent party in the last 40 years has won the election with the Index of Consumer Sentiment below 75. And only one incumbent, Barack Obama in 2012, won with the index below 90.

If you look at the far right portion of the chart, you’ll see the blue line showing actual consumer confidence has jumped the past two months, closing a sizable chunk of the anticipated-actual confidence gap.

The index still has a long way to go to get to 90, especially since history suggests we’re likely to see a drop next month. But as the above chart shows, the economy doesn’t have to improve for confidence to keep rising.

The explanation is simple: Inflation has been declining since June 2022. But consumers, shocked by the four-fold increase in monthly inflation in the year-and-a-half after Biden took office, have been understandably skeptical that the days of modest inflation have returned. With each passing month that produces stable inflation and continued modest job growth, a few more consumers begin to relax.

A look at the components of Michigan’s Consumer Sentiment Index reinforce this critical point. The index combines how consumers feel about the current economy and their expectations of the economy’s future. In January, as has been the case for months, consumers give a higher score to the current economy (83.3) than their expectations of the future economy (75.9). If the economy can avoid any major shocks in the coming months, look for that expectations number to start to catch up to the current economy number, further boosting the overall Consumer Sentiment Index.

None of this escapes Donald Trump and the right wing media that support him. They have been trying to convince Americans that the economy has been a disaster under Biden, and as the low Consumer Sentiment Index of the past year shows, they’ve been successful.

Will they continue to succeed as the economy hums along? Will the economy conveniently stumble to give their cries of economic Armageddon renewed credibility? The answers to these two questions very well might determine the winner in November.